Table Of Content

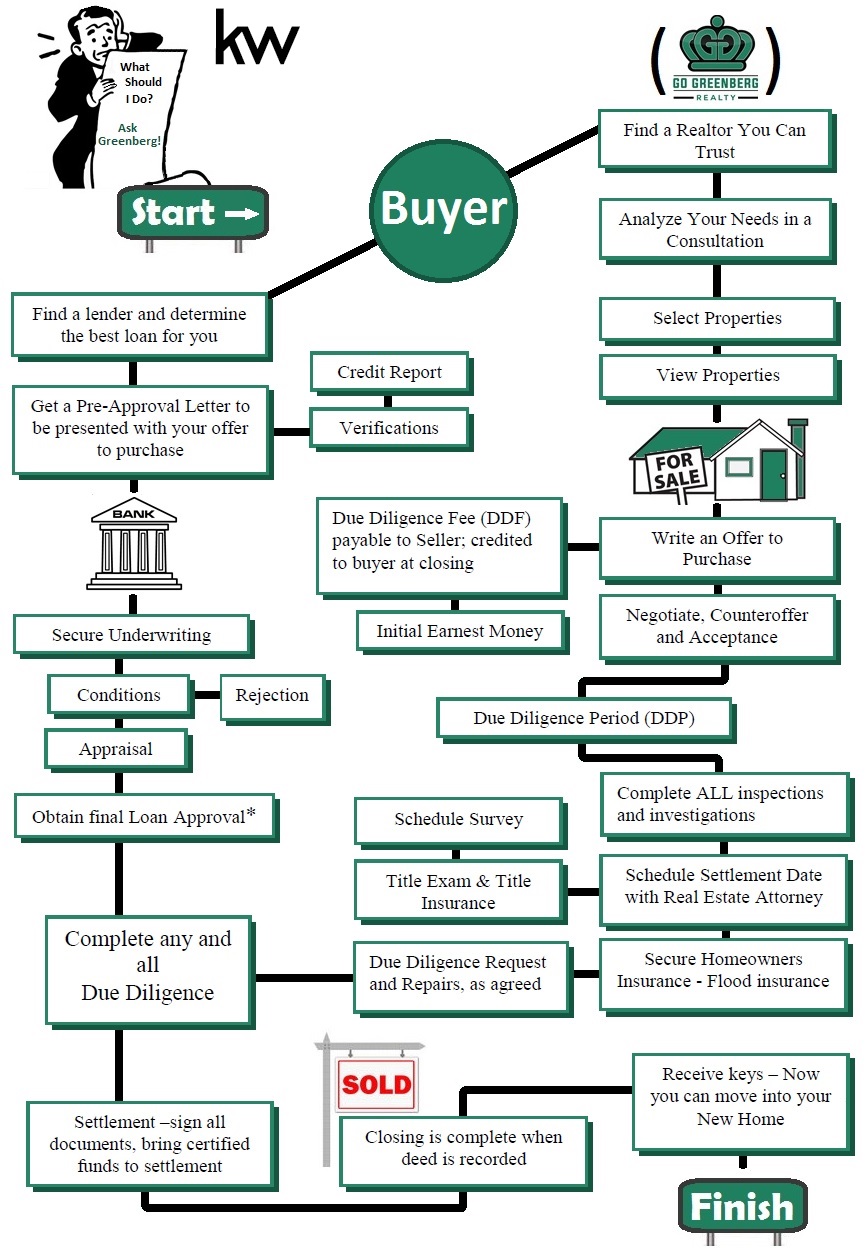

Regular maintenance can decrease your repair costs by allowing problems to be fixed when they are small and manageable. Paying down some of your debt or looking for ways to generate extra income before applying for a mortgage could help to improve your debt-to-income ratio. Mortgage credit requirements can vary depending on the type of home loan you’re trying to get. As stated up above, a conventional loan requires a minimum FICO® Score of 620, where an FHA loan requires as low as 580. The home inspection is important, as it will identify areas where major repairs or renovations require immediate attention as well as any work that needs to be completed in the future.

Closing day

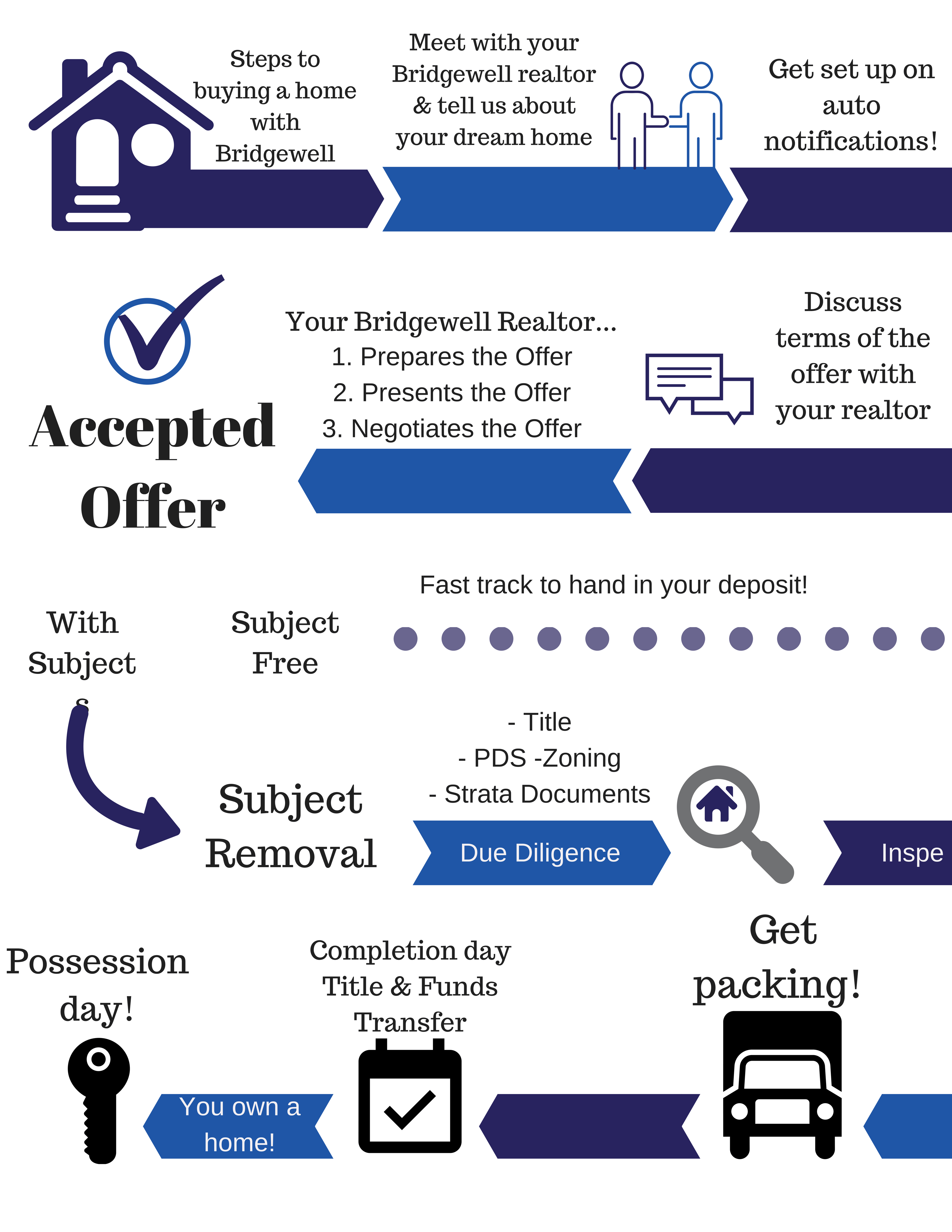

If you have a cosigner for your home loan, that person needs to be there. You’ll sign a settlement statement listing all costs related to the home sale. You’ll also sign the mortgage note, which states that you promise to repay the loan. Finally, you’ll sign the mortgage or deed of trust to secure the mortgage note.

Step 3: Call a real estate agent

Once you’ve submitted your loan application, it moves into processing. In this phase, your lender will give you a list of documents that you need to provide so they can verify all of the information you provided in your application. The quicker you submit them to your loan processor, the quicker your file will move along. Apply online for expert recommendations with real interest rates and payments.

Will that love letter help seal the deal — or add to housing discrimination?

When’s The Best Time Of Year To Buy A House? - Zing! Blog by Quicken Loans

When’s The Best Time Of Year To Buy A House?.

Posted: Thu, 08 Feb 2024 08:00:00 GMT [source]

In cases of multiple offers or a foreclosure, things could take a bit longer. Counter-offers are common and should even be expected when buying a house. Common counter-offers can include proposed changes to the price, closing date, or purchase contract contingencies. You may go back and forth with the seller a few times before you come to terms you both agree on. Once you’ve reviewed your Closing Disclosure, it’s time to attend your closing meeting.

From Better Money Habits

You can see how it might not work in your best interest to start dealing with a seller’s agent before contacting one of your own. Note that these are just the minimum required scores to qualify for a loan. Aim to have a higher credit score to be eligible for low interest rates. At this point in the home buying process, you’re probably eager to be done – but don’t neglect the final walkthrough.

This deposit is money you pay upfront to show the seller you’re serious about the offer and make them feel more comfortable taking their home off the market. If you’re having trouble finding a house that feels like home, consult your real estate agent. Agents aren’t just experts on helping people find a home; they’re also experts on the local housing market.

How Long Does It Take to Buy a House? - Realtor.com News

How Long Does It Take to Buy a House?.

Posted: Mon, 27 Nov 2023 08:00:00 GMT [source]

Money moves that can make a difference

Next, our technology will instantly match you with the best mortgage options available based on your information. And that’s it—you now have a free, no commitment pre-approval letter that gives you an accurate estimate of your homebuying potential. Once your mortgage is approved and at least three business days before you close, you will receive a closing disclosure. It lists the fees you must pay, which typically total 2 to 5 percent of the home price. Then, bring your ID and any payments that are due to the closing.

Once you’ve completed all the necessary work, the keys are yours. You’ll also need to save money to cover closing costs – the fees you pay to get the loan. Several factors determine how much you’ll pay in closing costs, but it’s best to prepare for 3% – 6% of the loan amount. This means if you’re borrowing $200,000 for your purchase, you might pay $6,000 – $12,000 in closing costs. While your title, appraisal, and inspection work is being completed, your lender will thoroughly review all the information you provided to verify that it is accurate.

The specific amount you’ll pay in closing costs will depend on where you live and your loan type. It’s a good idea to prepare to pay 3% – 6% of your loan amount in closing costs. In some situations, part or all of the closing costs can be rolled into your mortgage or paid by the seller as part of agreed-upon seller concessions. Debt-to-income ratio (DTI) is another factor mortgage lenders assess when considering your loan application. Your DTI helps your lender see how much of your monthly income goes to debt payments so they can evaluate the amount of mortgage debt you can take on.

You can also use local searches and read reviews of realtors on sites like Zillow. Once you've picked out a few of your top realtors, meet with them and see if they're a good fit for you. If you’re able to work out a deal with the seller—or better yet, if the inspection didn’t reveal any significant problems—then you should be ready to close.

Let’s now go over some final tips to make life as a new homeowner more fun and secure. Put out some feelers with your friends, family, and business contacts. You never know where a good reference or lead on a home might come from. Consider getting pre-approved for a loan before placing an offer on a home.

Here’s how you can put down less and get more help with down payment and closing costs. If you’ve never owned a home before — or if you haven’t owned one within the last three years — the California Housing Finance Agency considers you to be a first-time homebuyer. You’ll need to meet the state’s income limits and satisfy a range of other requirements, including completing a homebuyer education course.

From asking the right questions to negotiating tactics, get tips on how to make an offer on a property. House prices can go down as well as up and it can cost money to move. For example, if you’re hoping to start a family, finding a place with room to expand may mean you won’t have to sell to buy a bigger place later on. That's why I had the idea of sacrificing living in a larger space and moving into a small one. The main home's primary bedroom — the one I turned into a micro studio — is renting for $875. I'm charging the other tenant for the remainder of the house $1,305.

Financial health reflects the ability to live within one's means, save money and be able to afford all monthly obligations like loan payments and everyday expenses. Step one, as noted at the top of our list, is to check your credit score. Before you get into finding a lender, real estate agent or even looking at homes, you should take a look at where your creditworthiness stands.

A Decision in Principle is not a guarantee that your mortgage application will be accepted, but it can help you understand your options and what you may be able to afford. It also shows estate agents you’re serious about buying a property. When you apply to borrow money, lenders will look at your credit score before deciding whether to accept your application. It can show them how reliable you are at borrowing and repaying money. Some lenders, including HSBC, offer 95% mortgages that require a smaller deposit. There are also government housing schemes available to help make buying a property easier.

No comments:

Post a Comment